With the revolution of 401(k)’s in America, more workers than ever have become their own pension plan managers in an effort to protect their investments and ensure they’re in control of the risk management. But, as a growing number of people retire, they’re learning they need to convert their investment portfolios into income.

And it’s not as easy as you may think. Retirees can’t depend on bonds for income because the yields are so low, and if they bet too big on equities their savings could be jeopardized in a volatile market.

So what can you do?

A number of academics recommend whole life insurance as a form of maintaining your investment portfolio and building cash value. It can even boost your retirement income if used correctly!

The stable growth allowed by term life allows consumers to pursue high-risk, higher return strategies than other investments, while leaving more financial estate to their beneficiaries.

Let's take a look at the math.

“Wade Pfau, a professor of retirement income at the American College of Financial Services, compared a 40-year-old who buys term insurance and makes a large 401(k) contribution with an identical worker who buys a $500,000 whole life policy and makes a smaller contribution to his 401(k). Because the worker with whole life is building cash value in his policy, he or she can safely allocate a higher percentage of the 401(k) to equities than the other worker, Pfau says.

The upshot: At age 65, the worker with the whole life policy has a 401(k) account that is equal in size to the other worker in a buoyant market and 17% smaller in a bad market. In either scenario, Pfau calculates, the worker with whole life comes out ahead because he has $210,000 in cash value that he can borrow against in retirement.”

–Neal Templin, Financial Writer for Barron’s

All of that said, the benefits of bolstering a whole life insurance policy gives a retiree that ability to pivot, and not tap into their retirement funds during downturned markets.

How does Whole Life Insurance Work?

When you buy into a whole life policy, you’re purchasing a tax-free savings vehicle as well as a life insurance policy. Each year, a growing part of your premium goes into the savings vehicle while the cash balance grows tax-free at an interest rate that is guaranteed by the insurer.

- Whole life insurance pays dividends to policyholders on top of the guarantees

- Dividends increase your cash balance and death benefits

- You can borrow against your cash value, tax-free and don’t have to pay it back (but it will reduce your death benefits dispersed to your heirs)

Don't wait too long to buy.

The sweet spot for buying whole life insurance is from the ages of 35 to 45. This gives you time for the cash value to build up before retirement and reduces the risk of you being denied by a life insurance provider because of health issues.

Your premiums will also be cheaper because insurers will anticipate your to be around for a long time!

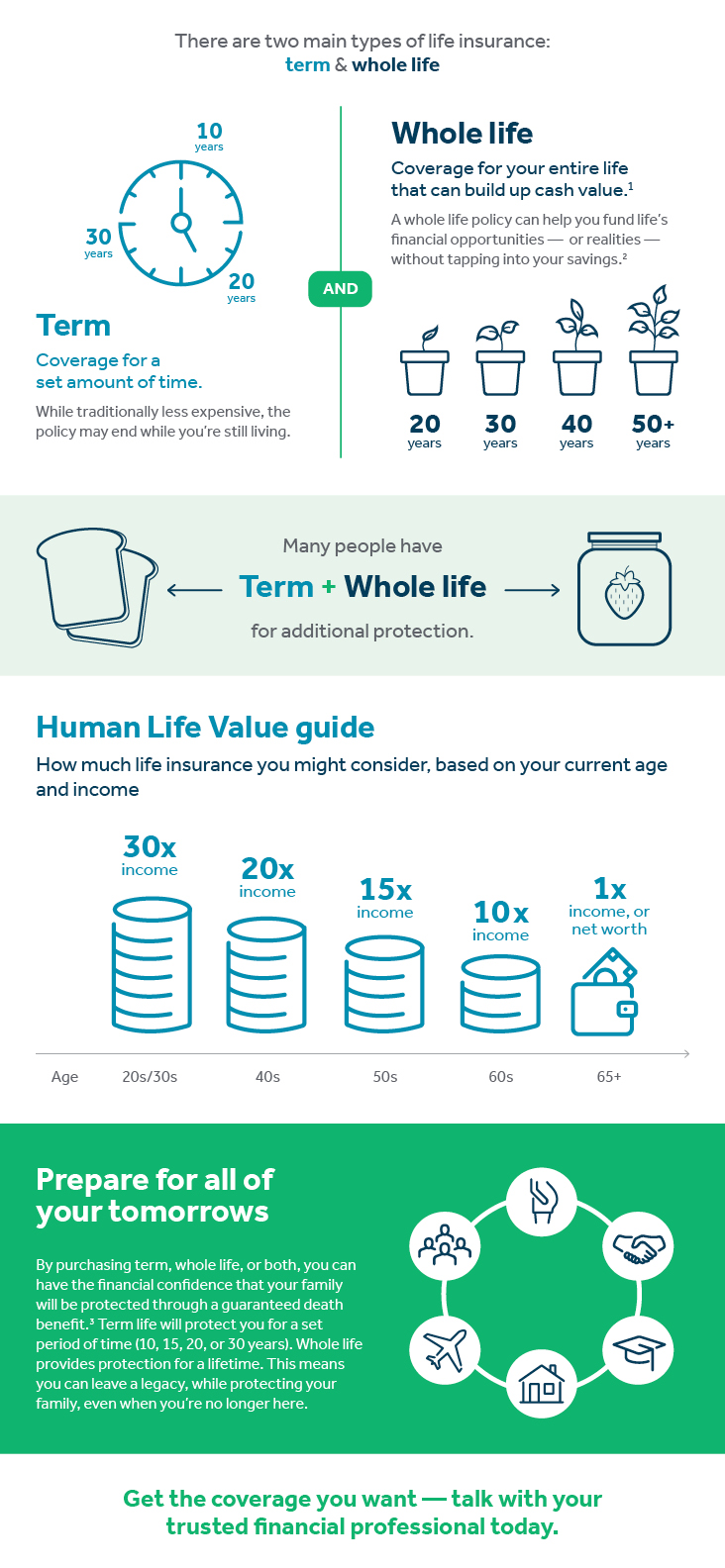

Get the best of both worlds by investing in term and whole life insurance.

Because whole life insurance contains a savings component and lasts your entire life, it is more expensive than term insurance which provides a death benefit only for a certain period of time.

By utilizing both term and whole life insurance, you’ll ensure your family is covered in the event your income is suddenly gone. And as you near retirement, you can simply let your term insurance expire, while your whole life insurance continues to grow.